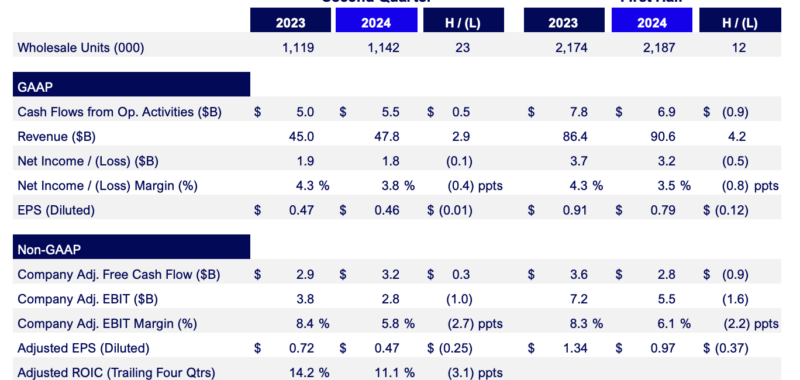

Ford reports second-quarter revenue of $47.8 billion, net income of $1.8 billion and adjusted EBIT of $2.8 billion

Customers exercising “freedom of choice” made Ford the No. 1 gas, No. 2 electric and No. 3 hybrid vehicle brand in the U.S. and the company remains confident in full-year 2024 results, including increasing effectiveness generating cash.

President and CEO Jim Farley said those are second-quarter outcomes resulting from further execution of the customer-centered Ford+ plan – with disciplined capital allocation setting the table for profitable long-term growth by a more strategically and financially durable company.

“Ford+ is on track, our underlying quality is improving, and Ford Pro is showing the huge upside we’ve got in all our businesses,” Farley said. “Transparency and accountability from having separate teams focused on the needs of different customers are leading to better decisions and greater value for everyone.”

Company Key Metrics Summary

Ford’s second-quarter revenue was $47.8 billion, up 6% year-over-year on a slight increase in wholesales. Benefits of a persistently fresh lineup of vehicles included momentum from the all-new F-150 pickup and record volumes of Transit commercial vans.

Company net income was $1.8 billion and adjusted earnings before interest and taxes, or EBIT, was $2.8 billion. Profitability was affected by an increase in warranty reserves, though efforts to lift the quality of new products are starting to pay off, with positive implications for customer satisfaction and Ford’s operating performance.

J.D. Power last month reported that Ford jumped 14 spots to No. 9 in the analytics company’s 2024 U.S. Initial Quality Study. Bronco Sport was named the best small SUV for initial quality; Ford’s Lincoln luxury brand was recognized for enhanced performance.

“Our own evaluations are showing similar quality gains,” said Ford Vice Chair and CFO John Lawler, “with declines in the number of incidents during the critical first three months in service, what the industry calls ‘3MIS.’”

Product launch and 3MIS data are leading indicators of future warranty costs, with today’s quality improvements typically showing up in financial results down the road.

“We still have lots of work ahead of us to raise quality and reduce costs and complexity, but the team is committed and we’re heading in the right direction,” said Lawler.

Operating cash flow in the second quarter was $5.5 billion and adjusted free cash flow was $3.2 billion. At quarter-end, Ford’s continually strong balance sheet had close to $27 billion in cash and about $45 billion in liquidity – supporting disciplined allocation of capital to invest in both long-term growth and returns to shareholders.

The company today declared a third-quarter regular dividend of 15 cents per share, payable Sept. 3 to shareholders of record at the close of business on Aug. 7.

Ford Pro’s second-quarter EBIT was $2.6 billion, an increase of 7% and a margin of 15%. Segment revenue was $17.0 billion, up 9% – three times the rate of growth in product shipments during the period.

Demand by commercial customers for Super Duty trucks and Transit commercial vans is outstripping production capacity. The ever-growing popularity of Super Duty and its strategic importance to Ford prompted the decision announced last week to add a third North America assembly plant to assemble the trucks.

Beginning in 2026, the company’s Oakville Assembly Complex in Ontario, Canada, will initially add capacity of up to 100,000 Super Duty trucks – and, in the future, a version with multi-energy technology – to volumes already being “Built Ford Tough” at the Kentucky Truck and Ohio Assembly plants.

Subscriptions to Ford Pro software were up 35% in the quarter and mobile repair orders fulfilled by the company’s fleet of about 2,000 service vehicles – and counting – more than doubled.

Business Segment Highlights

Farley said it’s common for commercial customers to adopt new technologies of all types – like connected, increasingly electric vehicles today – before individual consumers. Accordingly, advantages to customers and the company from the customer-focused segments defined by Ford+ are accruing first in that space.

“The capabilities we’re developing in electric vehicles and software-enabled and physical services are wide competitive moats between Ford Pro and other companies,” said Farley. “For customers, from small businesses to the largest enterprises, they’re bridges to transforming their organizations at the same time we’re remaking ours.

“Over time, we’ll build out those same kinds of benefits for Ford Blue and Ford Model e customers and further distinguish us from other automakers, traditional and new ones.”

Second-quarter wholesales and revenue for Ford Blue were up 3% and 7%, respectively, the latter to $26.7 billion. Truck volumes grew and overall pricing was strong. EBIT of $1.2 billion was down from the year-ago quarter, mostly because of the higher warranty costs.

Sales of hybrid vehicles increased 34% and accounted for nearly 9% of all Ford vehicles worldwide. That’s two full points higher than in second-quarter 2023 with more hybrid models of the company’s most popular products on the way.

Ford Model e had an EBIT loss of $1.1 billion amid ongoing industrywide pricing pressure on first-generation electric vehicles and lower wholesales. Those factors more than offset about $400 million in year-over-year cost reductions in the segment. Ford Credit had second-quarter earnings before taxes of $343 million.

Full-Year 2024 Outlook

With Ford+, Lawler said, the company is laying a foundation for profitable, long-term growth and, in the meantime, is on course for a solid full-year 2024 operating performance. Ford’s guidance range for adjusted EBIT remains $10 billion to $12 billion and expectations for adjusted FCF have been raised by $1 billion to between $7.5 billion and $8.5 billion.

Capital expenditures for the year are still anticipated to be between $8.0 billion and $9.0 billion, with an enterprise-wide objective for the lower end of the range.

Outlooks for full-year EBIT are up for Ford Pro, to $9.0 billion to $10.0 billion, on further growth and favorable product mix, and down for Ford Blue, to $6.0 billion to $6.5 billion, reflecting higher warranty costs than originally planned.

An anticipated full-year loss of $5.0 billion to $5.5 billion for Ford Model e is unchanged, with continued pricing pressure and investments in next-generation electric vehicles. Earnings before taxes from Ford Credit are expected to be about $1.5 billion, which would be a double-digit percentage increase from 2023.

Ford plans to report third-quarter 2024 financial results following the close of market on Monday, Oct. 28.

SOURCE: Ford